When consumers purchase a product, many things happen behind the scenes before that box hits their front porch. Manufacturers need to order materials and components for producing the product, receive them, house them in a warehouse, and assemble and distribute the final product.

During this process, there is a lot of data to keep track of, such as lot numbers, serial numbers, costs, quantities, expiration dates, etc. This data needs to be tracked and continually updated after every step to ensure efficient production.

Inventory management is the process of tracking and managing inventory from the time it is acquired to the time it is sold. Inventory includes raw materials, work in progress, and finished products.

Establishing an accounting system for inventory is essential to maximizing profit. In this article, we will discuss the entire inventory management process, from tracking raw materials and the benefits of implementing an inventory system. Additionally, we will walk you through selecting a system that works for you and your organization.

Benefits to Managing Inventory

There are many benefits to managing inventory and putting a system in place that is consistently updated when changes are made. Inventory management systems can help businesses track their inventory levels and prevent stockouts.

Inventory systems can also help businesses save money by reducing the number of raw materials and finished products that need to be stored while still ensuring enough product is on hand to meet demand.

Creating a consistent process will help businesses maximize their income by ensuring that finished products are sold quickly while preventing a surplus of stock from being moved.

Initial Steps

The first step in inventory management is acquiring and tracking raw materials. Raw materials can be purchased from suppliers or extracted from the environment. Once raw materials are received, they must be stored until required for production. Inventory systems track all raw materials’ quantity, location, and condition.

After receiving materials, they need to be stored in a warehouse or facility until it is time to assemble the final products.

During production, the process from storage to the assembly line is called work in process. Production can be done in-house or outsourced to manufacturers. In either case, inventory management systems track the progress of production and the finished products as they are completed. Integrating tools like visual CPQ (Configure, Price, Quote) can enhance inventory management by enabling detailed customization options during the production phase, ensuring that specific customer requirements are considered efficiently. Visual CPQ can streamline product configuration and provide a visual representation of the final product, reducing errors and ensuring accuracy in tracking work in process.

Once production is complete, the finished products must be stored until sold. It is essential to track all final products’ quantity, location, and condition. When customers purchase products, the system is updated to reflect the decrease in inventory after distribution.

Selecting a System

If you are interested in implementing an inventory management system in your business, keep a few things in mind. The central place to start is determining what type of system you want to use.

Inventory management systems can be either manual or automated. Manual methods are typically less expensive to implement, but they require more time and effort to maintain. Automated systems are the opposite, more expensive to implement, but they can save you time and money in the long run.

Additionally, it would be best to establish how often to update your inventory levels. Inventory levels can be updated daily, weekly, monthly, or quarterly. Updating stock levels more frequently will require more time and effort, but it can help you track your inventory better.

Inventory Accounting

Once you have decided on a system, you need to track three things:

1. Inventory Quantity – can be tracked through your method of choice, either manually or automated.

2. Cost of Inventory – includes the purchase price, transportation costs, and storage costs.

3. Value of Inventory – the inventory’s selling price minus the cost.

Choosing the right inventory valuation method is a crucial step as it can significantly impact your reported profitability. There are two main inventory valuation methods, LIFO (Last-In-First Out) and FIFO (First-In-First Out). These terms originate from when goods were moved around on shelves in stores. The method determines the price point of the product. An item can be sold at a higher price due to increased demand or at a lower price due to expiration, storage costs, etc.

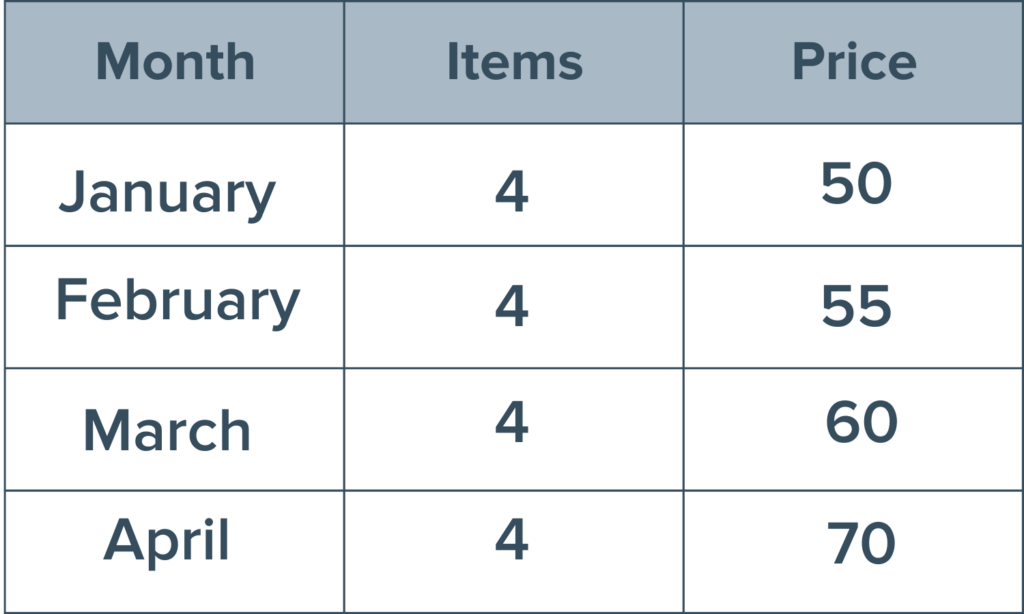

Here is a simple example to illustrate the difference between FIFO and LIFO. Let’s say a toy company buys and sells drones for kids. This company has purchased four drones per month in January, February, March, and April. However, due to inflation, the cost of the toy for the company got more expensive. There is a consistent cost increase for each successive month. Refer to the table below.

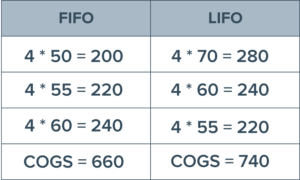

The toy company just got a shipment request for 12 drones. Refer to the table below to see the difference in COGS for the FIFO method compared to LIFO.

Using this example, the toy company would probably institute the LIFO method as this number reflects a higher inventory cost, meaning less profit and fewer taxes to pay at the end of the period.

Conclusion

Overall, inventory accounting aims to keep track of the cost of goods sold (COGS), which includes the cost of acquiring, storing, and selling inventory. COGS is a crucial metric for businesses because it directly impacts profitability. As a result, companies must carefully track their inventory levels and monitor their COGS to ensure they are maximizing profits.

Inventory management is an essential part of any business. Businesses must have an accurate picture of their inventory levels and costs to make informed decisions about purchasing, pricing, and selling products. This system is critical for any business that sells physical products; accounting for them consistently can be the difference between success and failure.

Learn more about accounting with FINSYNC’s cloud-based accounting platform to help you better manage your business operations.